Table of Content

Inquire about any processes or documentation required to pull money from your construction loan so that your contractor can use it. Construction-only loans can ultimately be costlier if you will need a permanent mortgage because you complete two separate loan transactions and pay two sets of fees. Closing costs tend to equal thousands of dollars, so it helps to avoid another set.

All loans assume that you meet the bank’s lending standards for debt-to-income ratio and credit score. At some point, you are tapped out and banks will not lend you additional money. For second mortgages, you will also need to have sufficient equity in your home. Typical loan limits are for 80% of the home’s value minus what you owe on the property. Most construction loans are issued by banks, not mortgage companies, as the loans are typically held by the bank until the building is complete.

Do construction loans cover the design phase of home construction?

This is called the “Subject to Completion Appraisal,” done by the bank. Unless you are paying cash for your project, you will need a construction loan to pay for the materials and labor, and you can use it to buy the land as well. Construction loans are a bit more complicated than conventional mortgage loans because you are borrowing money short-term for a building that does not yet exist. A construction loan is essentially a line-of-credit, like a credit card, but with the bank controlling when money is borrowed and released to the contractor. Homeowners secure this type of home renovation loan through lenders and brokers. There are also several key terms to know, and it’s important to know all parts of the deal before taking on a loan.

If you’re in the market for a construction loan let us help you make your dream home a reality. Generally, the bank makes the progress payments directly to the contractor after inspecting the job for completion of each phase of work. The final payment is usually endorsed jointly by you and the bank — a good idea so make sure this is your bank’s policy. This gives you some leverage to make sure the quality of the work is acceptable and that all punch list items are completed before releasing the final check.

Construction Loan FAQs

This can include private homes, retail centers, industrial buildings, and land acquisition. There are many types of construction loans available to individuals, businesses, and contractors to start and complete a project. If you exceed the approved loan limit, you will need to contribute cash, as you suggest.

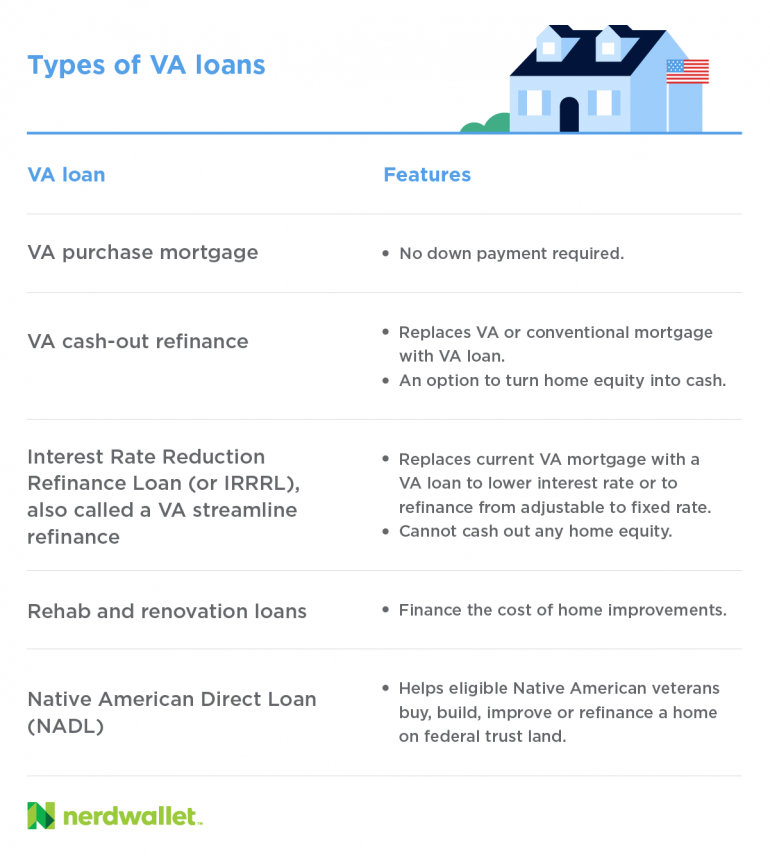

All in all, a construction-to-permanent loan is the more streamlined option, but not all lenders will offer this to all borrowers. Make sure to discuss both possibilities with your lender to figure out which one is right for you. A construction loan is short-term or temporary financing that funds your home build and is paid out through a series of installments as the construction advances. We offer VA home loan programs to help you buy, build, or improve a home or refinance your current home loan—including a VA direct loan and 3 VA-backed loans. Learn more about the different programs, and find out if you can get a Certificate of Eligibility for a loan that meets your needs. Construction-Only Loans are short-term and are considered specialty financing, with higher interest rates than a typical home loan.

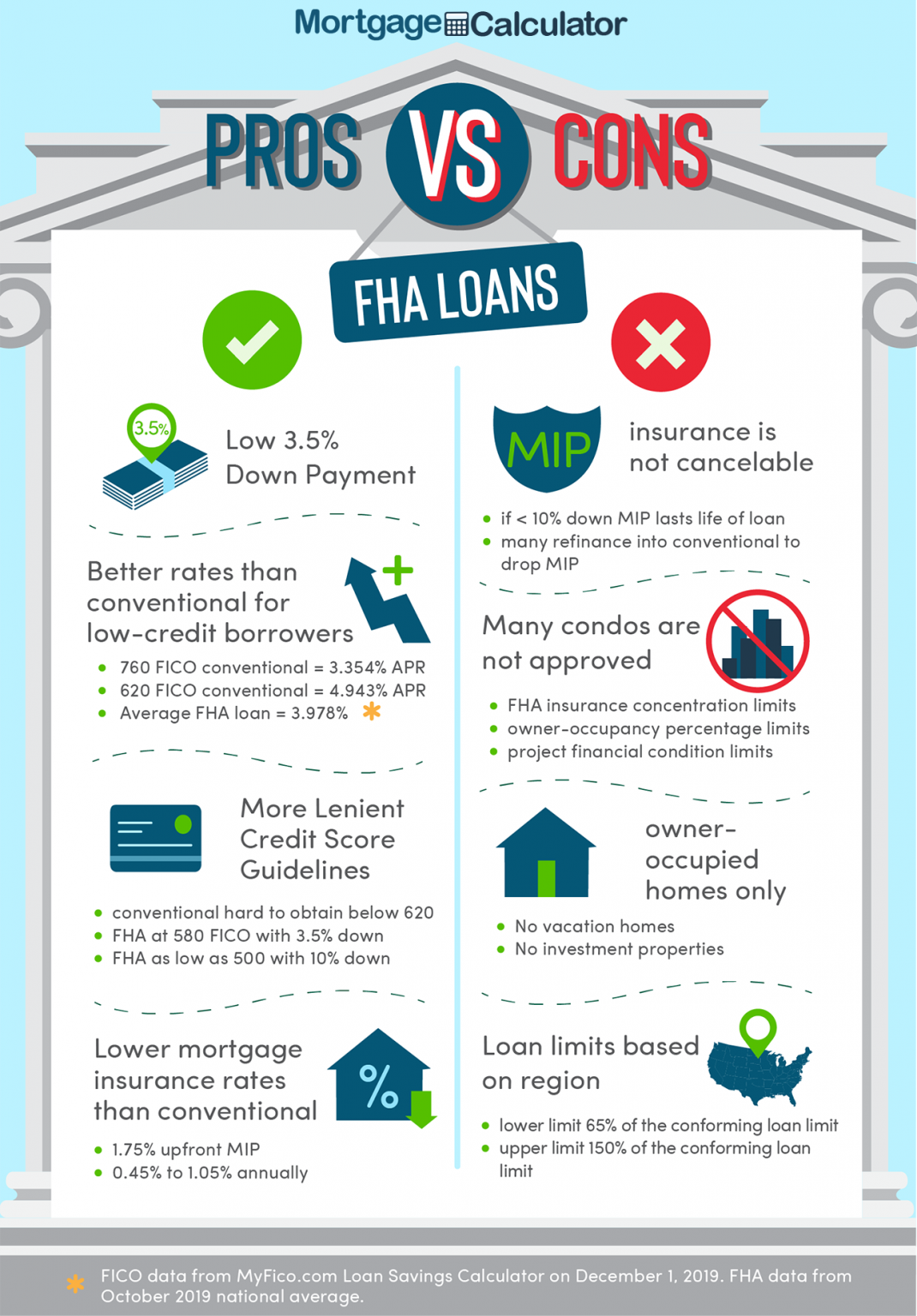

FHA Construction Loan

You will also need cash for closing costs, which tend to be high on construction loans, often 3% or more of the principal. Also, if your loan has an “interest reserve” that allows you to avoid interest payments during the term of the loan, some of the $400,000 loan will be used to pay interest rather than construction costs. A two-time-closing loan has a second closing when the home is completed, you have been issued a Certificate of Occupancy, and the contractor is fully paid. You will need to pay additional closing costs, but may get a better rate than a one-time close loan. Also, on some loans you are free to shop around for a better deal on the mortgage.

These loans can’t be used to purchase investment properties, and your home must meet the FHA’s lending limits. If you’re a first-time home buyer shopping for a home, odds are you should be shopping for mortgage loans as well—and these days, it’s by no means a one-mortgage-fits-all model. You’ll want to get and understanding of all the basics, with mortgage 101. While your home is under construction, you will be charged only interest on the amount disbursed to your builder, according to Quicken Loans.

It’s best to start early to get pre-qualified, then get quotes from at least three banks and credit unions for rates and closing costs. If you already have a banking relationship with a local bank, that’s usually the best place to start. Local banks and credit unions are often the best places to look for construction loans. With a two-close loan, you won’t know the interest rate on the permanent mortgage until you apply. If you think that interest rates are likely to rise, then locking in the rate with a one-time-close loan could work to your advantage. If interest rates are stable or falling, a two-time-close loan can be cheaper over the long run.

Interest-only mortgages require payments only on the interest charge of the home loan, and not on the loan principal itself, for an initial period . After that, payments go up substantially, as payments on the principal kick in. Renovation Loans, also known as 203 loans, can be used for home renovation and are insured by the Federal Housing Administration .

In addition they must approve the builder, the building plans, and appraised value of house when completed. A two-time-close construction loan, like you are describing, is like a line of credit with a balloon payment at the end. The full cost of the loan is any closing costs, including “points”, plus the interest payments. However, interest payments are only on the amount released, so they start very low and grow over time. Also, some banks allow you to delay all payments until the end of the loan, but that raises your loan amount since you are borrowing more to cover the interest payments.

If you already have a home, though, you might be able to use the proceeds to pay down the loan. An end loan simply refers to the homeowner’s mortgage once the property is built, Kaminski explains. A construction loan is used during the building phase and is repaid once the construction is completed. A borrower will then have their regular mortgage to pay off, also known as the end loan. The funds from these construction loans are disbursed based upon the percentage of the project completed, and the borrower is only responsible for interest payments on the money drawn. When you take out a construction loan, you’ll usually make interest-only payments while the construction is being completed.

Construction loans are also complicated if you are buying the land from one person and contracting with another to build the house. Unless you have detailed plans and a contractor ready to go, you will need time to finalize your plans and line up a builder. If you had chosen a variable rate, pegged to the prime or another benchmark, then you will have to pay the current rate at the time the mortgage converts. With a construction-to-permanent loan, you borrow money to pay for the cost of building your home, and once the house is complete and you move in, the loan is converted to a permanent mortgage. This option is attractive because you only have to go through the approval process ONE time, and you have only ONE closing and ONE set of closing fees. You don’t have to go back and do all of this again when you’re ready to secure permanent financing.

The maximum size of the mortgage will depend on your down payment , appraised value, your debt-to-income ratio, and credit score as with any other mortgage. If the new home, with land, is appraised at $500,000, it is likely you can likely borrow $450,000 if you qualify for a loan of this size. Your current lender should be able to provide additional details on their lending policies. In most cases, it’s best to start with your local bank, who often offer the best deals to existing customers and may be willing to get a little creative. If that doesn’t work out, check out credit unions and private mortgage companies, which may offer more options for marginal borrowers, but at higher rates and higher closing costs. Total closing costs, including the “origination fee” on a construction loan generally range from 2% to 3% of the loan amount.

The VA loan requires no down payment, no PMI, low closing costs, and no prepayment penalties. They can be fixed-rate or adjustable, and offer flexible refinancing. They also generally have a lower credit score threshold than many other loans. It’s worth noting that while borrowers don’t have to pay closing costs, they do have to pay a funding fee, which comes to 2.3% of the loan principal – either paid at closing, or rolled into the rest of the loan. And like USDA and FHA loans, VA home loans can’t be used for secondary residences or investments.

No comments:

Post a Comment